by Jin Wu

Stericycle Inc. (NASDAQ: SRCL), the Illinois-based world’s largest provider of regulated medical waste management, reported higher profits in both the fourth quarter and the year 2014 due to its successful acquisition strategy.

For the quarter ended December 31, Stericycle earned $82.5 million, or 96 cents per diluted share, compared with $78.2 million, or 90 cents per diluted share, in the year-earlier quarter. However, the diluted EPS missed the $1.12 consensus estimate of seven analysts, and the stock dropped 2.48 percent.

On an adjusted basis, which excluded elements such as acquisition and restructuring expenses, the company earned $1.12 per diluted share, up from 99 cents per diluted share, in the year-earlier quarter, equalling the consensus estimate of $1.12 by 16 analysts.

In the fourth quarter, revenues increased 19.2 percent to $676.9 million from $567.9 million.

For the 2014 fiscal year, Stericycle’s net income climbed 4.8 percent to $326.5 million from $311.4 million. Earnings per diluted share increased to $3.79 from $3.56, missing the consensus estimate of $3.95 per diluted share. Adjusted diluted EPS increased to $4.27 from $3.75, topping the consensus estimate of $4.26.

Full year 2014 revenues were $2.56 billion, up 19.3 percent from $2.14 billion.

Acquisitions greatly contributed to Stericycle’s fourth-quarter and full year performance. “In the quarter, we closed nine acquisitions, five domestic and four international. The revenues from the nine acquisitions were $7 million in the quarter and annualized approximately $43 million,” said Brent Arnold, chief operating officer of Stericycle, in the conference call. According to the press release, combined with previously completed acquisitions, total acquired revenue growth was $93.1 million in the fourth quarter.

“In 2014, we expanded our international operations completing 27 acquisitions in 10 countries including a new geography — South Korea,” Arnold said.

Al Kaschalk, analyst at Wedbush Inc., said because the majority of the acquisitions were executed internationally, volatility in foreign currencies became an inevitable factor influencing Stericycle’s earnings. In the press release, the management stated that there was unfavorable foreign exchange impact of $17.0 million in the fourth quarter and $33.6 million in the full year.

However, strong international growth offset the foreign-exchange headwind. Morningstar Inc. analyst Barbara Noverini said: “I think Stericycle just showed that their expansion strategy continued to work. That’s especially true with the strong internal growth rate that they posted to their international segment. It’s clear to me that all the acquisition they’ve been doing internationally, including some of the services they’ve managed to overlap the existing footprint internationally, are working because we start to see internal growth rate strengthened even further.” Stericycle’s international revenues were up 19.3 percent in 2014 and the company anticipates an internal growth rate of 6 to 9 percent in international markets in 2015.

For 2015, Stericycle lowered its expectation of diluted EPS to $4.63 to $4.69 per share, to account for the foreign-exchange impact. According to William Blair & Co.’s estimation, currency is expected to reduce total 2015 revenue by about $70 million.

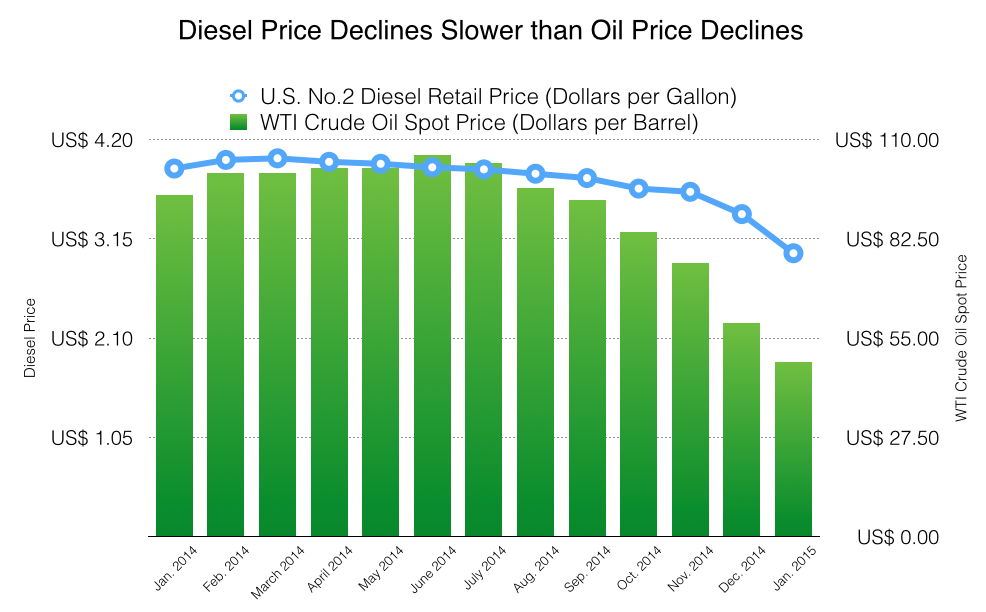

However, William Blair & Co. expects diesel price declines would benefit Stericycle’s margins modestly in early 2015.

The stock dropped to $131.62, down $3.35.