By Yemeng Yang

Wall Street is divided about the stock of Tesla Motors Inc., even as investors are cheering the electric car maker’s prospects under the new administration.

Shares of Tesla closed at $254.47 Wednesday, down 14 cents or 0.05 percent. But the stock has soared $59 or 30 percent since the election.

Analysts look askance. Their average 12-month target price on Tesla’s shares compiled by Bloomberg is $245.5, 3.5 percent lower than their latest close, with a wide range from $155 to $338.

Out of 24 analysts covering Tesla, eight rate the stock a buy, ten call it a hold, and six say sell.

“I can’t justify buying the stock because of the volatility and the fact that most of its outlook is way out to the future and we have very little near-term visibility,” said Ivan Feinseth, chief investment officer of Tigress Financial Partners LLC, in a phone interview.

“In spite of an impressive set of products and early leadership in the field of vehicle electrification, we see Tesla shares as overvalued,” wrote Brian Johnson, an analyst at Barclays, in a research note. His price target for Tesla is a mere $165.

Morgan Stanley last Thursday raised its target for Tesla to $305 from $242 and upgraded the company to overweight from equalweight.

“Vehicle electrification is accelerating broadly. The market is moving Tesla’s way,” wrote Adam Jonas, an analyst at Morgan Stanley, in a research note.

Tesla’s recent surge benefited from the new administration in Washington, and the company may continue to be a beneficiary given its net exports from the U.S. and higher percentage of U.S. content than any other car manufacturer.

Elon Musk, chief executive officer of Tesla, joined President Donald Trump’s economic advisory team as a strategic advisor in December.

“While we cannot explicitly apply a monetary value to this relationship, we believe this level of coordination with the new administration could actually evolve into greater strategic value than with the prior administration,” wrote Jonas.

Analysts anticipate Tesla’s net loss for the year ending Dec. 31, 2017, will be narrowed to $495.2 million, or $3.27 per diluted share, compared with an estimated net loss of $632.5 million, or $4.62 per diluted share, in 2016. Tesla is expected to earn money as early as 2018.

Deliveries of existing models and the production of upcoming Model 3 are two keys for Tesla to turn a profit.

The company is projecting to produce a total of 500,000 electric cars annually by 2018, including the luxury Model S sedan, Model X sport utility vehicle, and upcoming Model 3 mass-market sedan, which would be launched in late 2017.

In order to achieve the production target, in 2014 Tesla built a factory in Nevada to produce lithium ion batteries. The company calls it the Gigafactory. Investors were invited to tour the Gigafactory earlier this month.

“The Gigafactory is progressing faster than we had expected and is already manufacturing critical components/models for the Modal 3,” wrote Jonas, who later revised his Model 3 volume estimate upward, with a significant positive impact on his earnings estimate and price target.

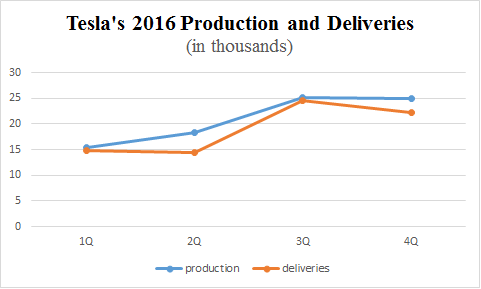

However, Tesla’s deliveries last year cast a shadow over the company’s production ability.

Tesla revealed this month that it had delivered only 22,200 vehicles in the fourth quarter due to short-term production challenges. Total 2016 deliveries were 76,230, missing the target of 79,000, which is already a reduction from the 80,000 to 90,000 it originally hoped to deliver.

“Next car is going to come out at the end of the year. Unfortunately, their ability to deliver on time has been challenged in the past,” said Feinseth.

Tesla missed its 2016 full-year delivery target amid its production ramp-up.

Tesla’s profitability hinges on how well its plans are executed.

“Our Underweight rating considers notable investment positives, including a highly differentiated business model, appealing product portfolio, and leading-edge technology, though which we believe are more than offset by above-average execution risk and valuation that seems to be pricing in a lot,” wrote Ryan Brinkman, an analyst at J.P. Morgan, in a research note.

Tesla shareholders approved the acquisition of SolarCity Corp., a solar energy provider, last November. The task of integrating the two companies, including products, brands and employees, lies ahead.

Morgan Stanley said it is too soon to tell if the acquisition adds any material value to shareholders.

J.P. Morgan significantly lowered its forecast of Tesla’s per-share earnings from the fourth quarter of 2016 onward, as SolarCity has reported an adjusted net loss of $759 million for the first three quarters of 2016, a trend J.P. Morgan expect to continue.

Tesla will release its fourth-quarter earnings in February.