By Ashesha Mehrotra

Wal-Mart Stores Inc. shares weakened Thursday after the retail giant, citing the impact of a strong dollar and planned store closures, trimmed its sales outlook for the year.

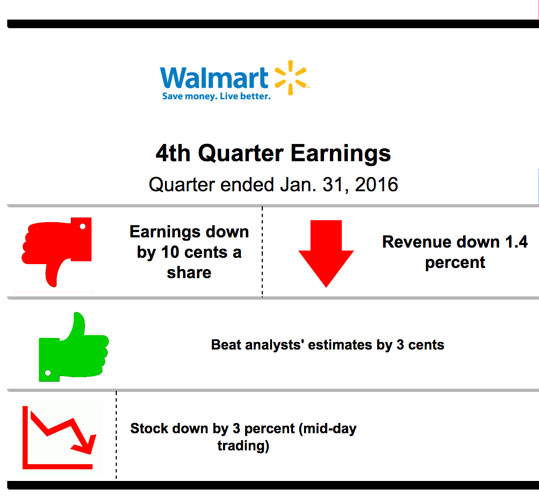

In the quarter ended Jan. 31, the Arkansas-based company had net income of $4.5 billion, or $1.43 per diluted share, down from $4.9 billion, or $1.53, in the year-ago period.

Revenues declined 1.4 percent to $12.9 billion from $13.1 billion reported last year in the same quarter.

Excluding non-operating items, the company said, adjusted earnings were $1.49 a share, versus $1.69 in the year-ago quarter. The latest quarter’s earnings beat by 3 cents the $1.46 a share analysts surveyed by Yahoo Finance had been anticipating.

In late-afternoon trading Thursday, shares of the nation’s largest retailer were down $2.12, or 3.2 percent at $63.99. Earlier in the day, the stock had fallen by as much as 5 percent.

Wal-Mart Stock Price Jan.2015-Feb.2016

[field name=”chart”]

Despite the better-than-expected profit performance, Edward Jones analyst Brian Yarbrough expressed concern about how investors would interpret the company’s results.

“The company beat earnings due to a lower–than-anticipated tax rate, which is kind of low quality,” he said. “The bigger issue is same-store-sales at Walmart U.S. were only up 0.6 percent versus expectations for 1 percent.”

Wal-Mart investors were less interested in the company’s solid earnings than they were in a cautious sales forecast the company issued. Previously, the company had estimated a growth of 3 to 4 percent. But on Thursday officials said sales will be relatively flat, due to currency headwinds and store closures. On a constant currency basis, the company said, the 3-4 percent growth will remain unchanged.

Despite the unwelcome news, some analysts believe investors should not worry about the temporary loss in share price as the company has a concrete plan of action in line.

“A key factor behind our thesis is that Wal-Mart’s brand, despite much negative publicity, still drives traffic,” said Ken Perkins, analyst at Morningstar.

Perkins said that the company’s fourth-quarter results show U.S. same-store sales’ traffic increased 0.7 percent, representing the fifth consecutive quarter of traffic increases. Also, the U.S. same-store sales increased for a sixth consecutive quarter.

The company continues to struggle in driving sales growth, against background of stern competition from retailers such as Amazon, which could imply a lowered guidance for their longer-term earnings guidance provided back in late 2015.

Sales growth for Sam’s Club, the company’s membership-only chain selling grocery items, electronics and more, had been expected to show a positive 0.5 percent, but dropped to negative 0.5 percent instead.

CEO Doug McMillon, however, responded positively to such concerns in a prepared statement. “We are pleased with fundamental trends that are allowing us to improve our stores, add critical capabilities and deepen our digital relationships with customers. Our initiatives are making it simpler and more convenient for customers to shop at Walmart.”

For the full year, the company said net earnings dropped 9.2 percent to $14.6 billion, or $4.57 a share, in comparison with the year-earlier income of $16.1 billion, or $5.05 per share. Revenues went down by just 0.7 percent to $48.2 billion from the previous year’s $48.5 billion.