By Urvashi Verma

Exxon Mobil Corp.’s new CEO Darren Woods announced that the company will spend more on refining operations and acquired projects such as those in the Permian Basin. But the moves aren’t enough to change analysts’ pessimistic forecasts for the company, as higher oil prices hurt the bottom line.

Exxon will increase its spending on capital projects to $25 billion, after two years of declining investment, Woods said at a meeting with analysts last week. The move follows the acquisition of companies controlled by the Bass family, announced in January, that more than doubled Exxon’s shale oil footprint in the Permian Basin.

“This acquisition strengthens ExxonMobil’s significant presence in the dominant U.S. growth area for onshore oil production,” Woods said in the company’s press release.

But based on the steady rise in oil prices, and stiff competition in U.S. shale production, many analysts are holding to the view that the company’s growth will be slow.

“I continue to see it lagging peers, with oil gradually rising in coming months, much like it has over the last year,” said Brian Youngberg senior energy analyst at Edward D. Jones & Co, in an email following the analyst meeting.

“The 2020 guidance for production volumes was increased slightly, mostly due to its recent acquisition in the Permian, but [I expect] limited other changes and no big strategic change with the CEO change,” Youngberg said.

Profit dropped 36.6 percent in the fourth quarter as the company wrote down its non-performing natural gas assets and had weaker profits from its refining operations.

Shares of the Irving, Texas-based company have taken a hit on the weaker profit picture. Since December the stock has decreased 11 percent to $82.39 and remains near its 52-week low of $80.93 set last month.

Exxon’s shares have declined 2.5 percent over the past 12 months, compared with the Standard and Poor’s 500 gain of 18.41 percent.

The average target stock price within the next 12 months is $89.50, based on analyst expectations compiled by Bloomberg, far below the 52-week high of $95.21 set in July.

“Bullish oil prices do not bode well for Exxon. It has massive refining and chemical operations,” said Pavel Molchanov. senior vice president and equity research analyst at Raymond James & Associates. “Oil producers with high operating leverage will perform better in this environment,” he added.

In a rising oil price environment, Exxon’s large refining and chemical businesses, when compared with its smaller exploration and production division, incur higher productions costs that put its profit margins under pressure.

Most of the company’s revenue, 76.6 percent, is generated from refining operations. Chemical operations generated 13.2 percent of Exxon’s 2016 revenue and 10.2 percent were from exploration and production.

Exxon’s concentration in refining and chemicals reduce its ability to maneuver between segments to maximize profit when oil prices are rising, analysts said.

In the past six months, the price of crude oil has increased 26.6 percent to $53.20 per barrel from $42 per barrel. West Texas Intermediate crude oil for April delivery stood at $53.26 per barrel in Tuesday morning trading.

Crude oil prices are expected to remain in a range of between $50 and $60 per barrel in the next year, based on analysts estimates compiled by Reuters.

Exxon’s trailing price-to-earnings ratio of 34.82, compared with 22.14 for the S&P 500, suggest to some analysts that its stock is overvalued.

“We have a sell rating on the stock because it is unattractive compared to its peers,” said Molchanov.

Of the 29 analysts surveyed by Bloomberg, just four suggest that investors buy shares of Exxon, 19 suggest neither buying nor selling the shares, and six have a “sell” rating on the stock.

A major factor impacting the company’s profitability has been recent write-downs and prescribed changes by the U.S. Securities and Exchange Commission requiring companies to take oil and gas reserves off their books if they aren’t profitable at existing prices.

In January, Exxon took a $2 billion dollar write-down of its natural gas assets, a primary reason the company missed analysts’ earnings expectations in the fourth quarter.

Exxon announced late last month that it took a 3.3 billion barrel net reduction in its oil equivalent barrels, a term used to summarize the amount of energy equivalent to the amount of energy found in a barrel of crude oil.

This included 3.5 billion in bitumen in Kearl Alberta and 800 million oil- equivalent barrels in North America, which were offset by Exxon adding 1 billion barrels of new oil and gas reserves in the United States, Kazakhstan, Papua New Guinea, Indonesia and Norway.

“Certain quantities of liquids and natural gas no longer qualified as proved reserves under SEC guidelines,” Exxon said in a press release.

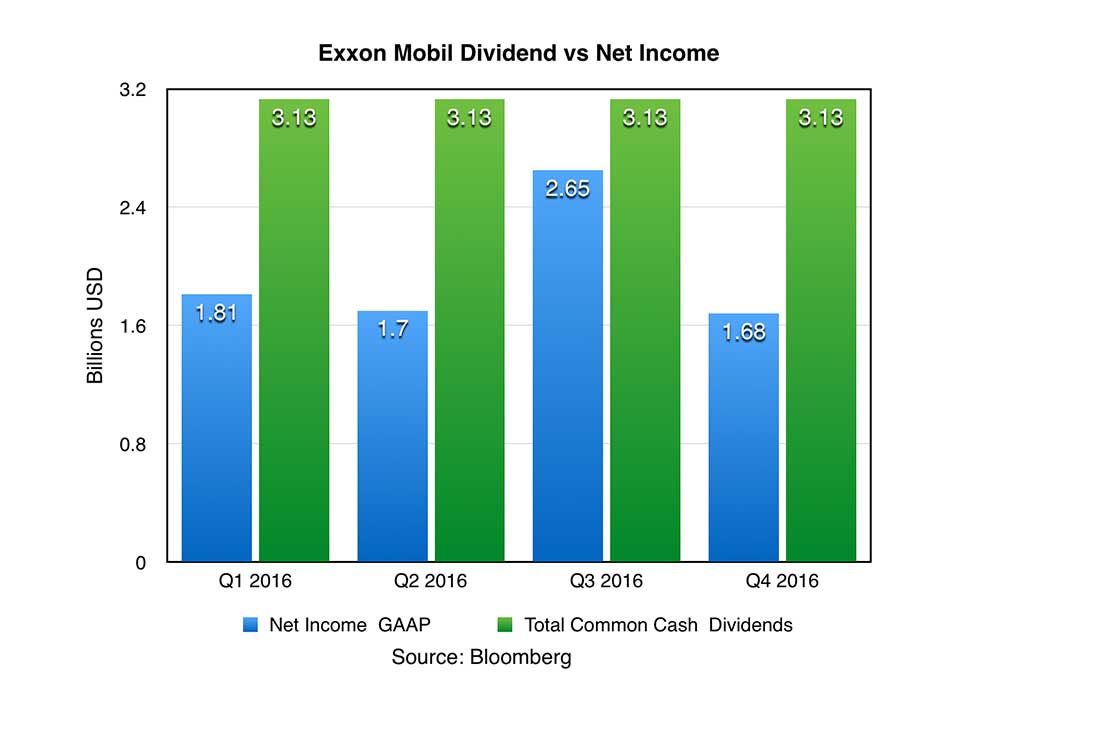

Despite Wall Street’s diminishing patience for the giant, Exxon remains a favorite among small shareholders. The company has earned a reputation for paying out fat dividends and has increased the annual dividend for 34 consecutive years.

Exxon raised its dividend by 3.5 percent to $2.98 in 2016, a move that has not landed as positively with Wall Street analysts, as the company paid more in net common dividends to shareholders than it generated in net income in all four quarters, according to financial filings.

“This path is unsustainable. Exxon is paying out more in dividends than it takes in profits,” Youngberg said.

While dividends are not in jeopardy, Exxon announced in its most recent earnings conference call that it will stop repurchasing its own shares except to offset dilution. Exxon has spent $210 billion over the last decade buying back its own stock.

Meanwhile, the company’s debt continues to mount. From 2012 to 2016 Exxon’s short- and long-term debt has more than tripled to $39.37 billion from $10.54 billion, according to financial statements.

Last year, Exxon lost its AAA Standard & Poor’s credit rating and was downgraded to AA+. The company was warned it could be downgraded further if it continues to add more debt in order to pay for acquisitions or dividends, without cutting costs.

But not all analysts agree with the downbeat outlook.

“It was a tough year for them. Last year [Exxon] wasn’t able to address many issues due to an expected change in management and with new management, many of these issues will be resolved,” said Sam Margolin, managing director of equity research at Cowen and Company, in an interview.

Darren Woods became CEO of Exxon in January after Rex Tillerson stepped down to become U.S. Secretary of State in the Trump administration. Some analysts are skeptical that new management will be able to shift the tide for Exxon.

“Since the CEO change, we’ve heard the theory that Woods, having come out of Exxon’s downstream operations, will pivot in that direction,” said Molchanov in a note following the analyst meeting. “In reality, there is no pivot, because Exxon over the past decade has been more committed to remaining a true integrated company than any of its peers.”

Two major exploration and production projects expected to lift Exxon’s bottom line are the Papua New Guinea project and Delaware Basin acquisition.

Exxon’s liquefied natural gas field in Papua New Guinea has a new natural gas discovery expected to produce approximately 6.9 million tons of liquified natural gas per year. It is geographically positioned to serve energy demand in Asia. One of its major customers is China Petroleum & Chemicals Corp.

Photo at top: Exxon Gas Station in Durham CT ( Mike Mozart via Flickr)